A bank reconciliation statement is a document that compares a company’s bank account records and financial records. This is to ensure that both company records and bank statements are in agreement. It is a crucial process that helps businesses to identify and resolve any discrepancies between the two sets of records.

Methodology – How Bank Reconciliations Are Prepared

The methodology for preparing a bank reconciliation statement typically involves the following steps:

- Gather the necessary documents: The accountant will need to gather the company’s checkbook and bank statement, as well as any other relevant documents, such as deposit slips or bank fees and charges.

- Compare the company’s records with the bank’s records: The accountant will compare the company’s records with the bank’s statement, and identify any discrepancies between the two. This may include checks that have been written but not yet cleared by the bank, deposits that have not yet been credited to the account, and bank fees or charges that have not yet been reflected in the company’s records.

- Investigate and resolve outstanding items: The accountant will need to investigate the cause of any discrepancies and take appropriate action to resolve them. This may involve contacting the bank to resolve the issue or making adjustments to the company’s records.

- Prepare the bank reconciliation statement: Once all outstanding items have been resolved, the accountant will prepare the bank reconciliation statement, which will include a comparison of the company’s records with the bank’s records, as well as any necessary adjustments.

- Review and approve the reconciliation statement: The accountant will review the reconciliation statement to ensure that it is accurate and complete. Once it has been reviewed and approved, it can be filed with the company’s financial records.

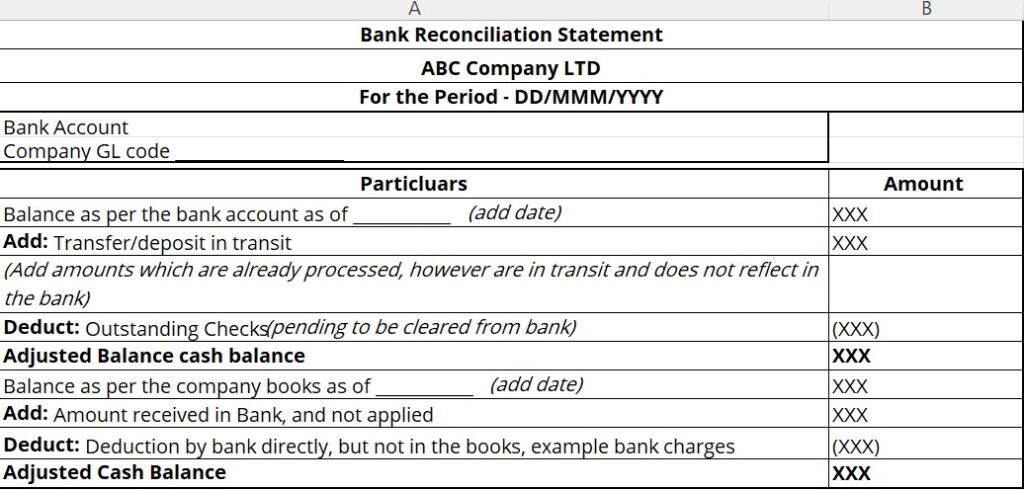

We have attached a FREE downloadable and editable Bank Reconciliation Statement Template. Download your copy now.

Bank Reconciliation Statement - A Template

Send download link to:

Team MKBS provide Business and Financial consultancy and advisory to SMEs. Contact us on contact @mkbsindia.com for any inquiries and support. Also we provide a FREE face to face (one time) consultation on any Business related matters.

Identifying and Resolving Outstanding Items in a Bank Reconciliation Statement

There are several possible outstanding items that may appear in a reconciliation statement. These may include:

- Checks that have been written but not yet cleared by the bank: These checks will appear in the company’s records as having been paid, but will not yet have been reflected in the bank’s records.

- Deposits that have not yet been credited to the account: If a company has made a deposit but it has not yet been credited to their account, it will appear as an outstanding item on the reconciliation statement.

- Bank fees or charges that have not yet been reflected in the company’s records: If the bank has charged the company a fee or charge, it will appear as an outstanding item on the reconciliation statement until it is reflected in the company’s records.

In order to resolve discrepancies in a reconciliation statement, accountant must identify cause of outstanding items and take corrective measures. This may include reaching out to the bank or adjusting the company’s financial records to accurately reflect the information.

For example, to address discrepancies in reconciliation statement, accountant may reach out to bank to clarify status of outstanding items. This includes verifying the processing of a check that has not yet been cleared, ensuring that a deposit has been credited to account, or adjusting company’s records to reflect a fee or charge that has been assessed by the bank. These actions help to resolve outstanding items and maintain the accuracy of the company’s financial records.

Frequency In Preparation Of Bank Reconciliation Statement

The frequency in which a bank reconciliation statement is prepared will depend on the policies of business. Some companies may prepare a bank reconciliation statement on a monthly basis, while others may do so quarterly or annually.

There are several factors that can influence the frequency with which a reconciliation statement is prepared. These may include:

- The size and complexity of the business: Larger, more complex businesses may require more frequent reconciliation statements to ensure the accuracy of their financial records.

- The company’s internal policies: Some companies may have established policies or procedures that dictate the frequency with which a reconciliation statement should be prepared.

- Regulatory requirements: Businesses may be required by law to prepare and maintain a bank reconciliation statement on a specific frequency. For example, publicly traded companies are typically required to prepare a reconciliation statement as part of their annual financial statements.

Advantages of Regularly Preparing a Bank Reconciliation Statement for SMEs

There are several benefits of preparing a bank reconciliation statement for small and medium-sized enterprises (SMEs):

- Accuracy of financial records: The statement helps to ensure the accuracy of a company’s financial records by comparing them with the bank’s records. This helps to identify and resolve any discrepancies, which can prevent errors and reduce the risk of financial mismanagement.

- Resolution of issues: Preparing bank reconciliation statement can help SMEs identify and timely resolve issues with their bank accounts. This can help to prevent overdrafts, late fees, and other costly problems that can arise from mismanagement of accounts.

- Maintenance of good relationships with banks: By demonstrating a commitment to financial accuracy and responsibility. SMEs can build trust with their banks and potentially secure more favorable terms on loans and other financial products.

- Compliance with regulations: In some cases, SMEs may be required by law to prepare and maintain a reconciliation statement. By regularly preparing a bank reconciliation statement, SMEs can ensure that they are in compliance with these regulations.

- Improved financial management: SMEs can gain a better understanding of their financial situation, including cash flow, profitability, and financial risk. This can help businesses to make informed financial decisions and improve their overall financial management.

Conclusion

Ensuring that both your bank statements and your accounting records match is an important part of maintaining your company’s finances. After all, a complete and accurate accounting of your company’s financial status will help you to make informed decisions. If there are discrepancies between the two sets of records, consider hiring an outside professional to audit your books.

The statement helps you spot any mistakes or errors in your bank balance and correct them. It is also helpful if a business needs to know how much money is in the bank during a period. A reconciliation statement is vital when you have more than one bank account. Ensuring that all accounts are accurate and up to date is essential for every small business.